THE BIG BEAUTIFUL BILL AND THE UGLY MATH BEHIND IT

A Rational Look at Who Is Actually Paying More

I was three cups deep into a Thursday morning scroll when it hit me. Not a headline. Not a hot take. A pattern. The same talking points, recycled across platforms, repackaged in different fonts, pushed by accounts that may or may not be operated by actual humans. Lower taxes. Bigger refunds. The economy is booming. Trust the math. Except nobody was showing the math. They were showing the vibe.

So I did what any rational person should do when the noise gets louder than the signal. I closed the apps. I opened the spreadsheets. I went ole-school.

I grew up in a house in Moraga, California, where every Sunday morning meant one thing. My Mom, MJ, at the kitchen table, checkbook open, bills fanned out like a hand of cards she intended to win. The envelopes were sorted by due date. The register was filled out in pen, not pencil, because pencil meant you were leaving yourself room to lie. She had a Texas Instruments calculator next to the checkbook, and before that, before the calculator even existed in our kitchen, she did it by hand. Arithmetic. Long division on scratch paper. Columns that added up because she made them add up. She would run the numbers, check them twice, and only then would she write a check. And the rule, the one rule that governed that kitchen table like scripture, was simple: you do not write a check your account cannot cash.

That was not a political philosophy. That was not liberal or conservative. That was arithmetic. The kind you do with a TI calculator, a bank statement, and the lights on. The kind that does not care who you voted for, who you follow, or which cable news anchor makes you feel like you are on the winning team.

I ran the numbers this week. On the One Big Beautiful Bill Act, on the tariffs, on the proposed budget, on the national debt, and on the interest payments we owe just to keep the lights on. I did it the way MJ would have. Bills on the table. Calculator out. No spin. No tribal math. Just the ledger.

And the ledger, to put it the way she would have, does not balance. Not even close.

THE BIG BEAUTIFUL BILL: WHAT IT ACTUALLY DOES

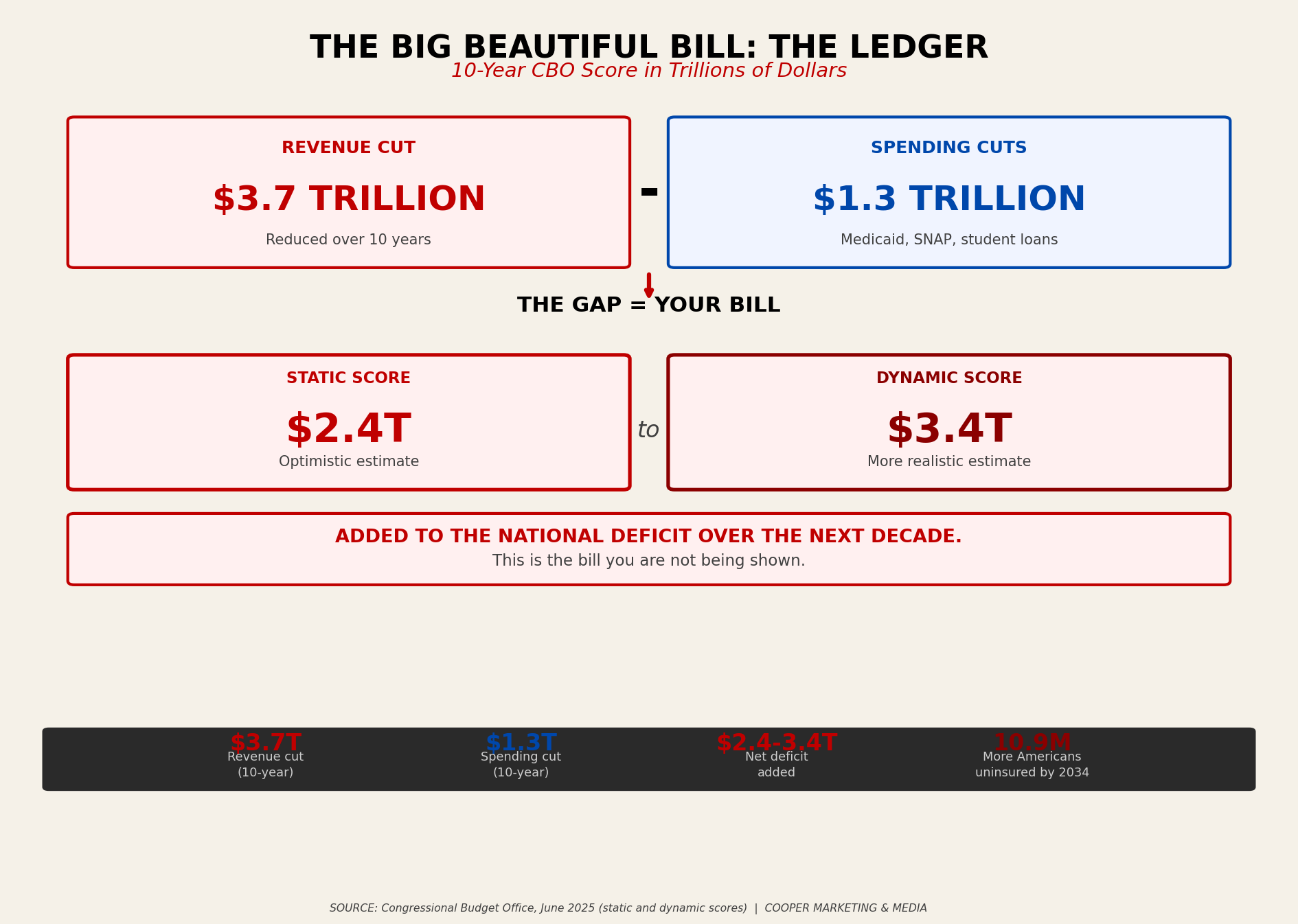

The One Big Beautiful Bill Act, signed into law in late 2025, is the largest tax and spending package in a generation. It permanently extends the 2017 Tax Cuts and Jobs Act provisions that were set to expire on December 31, 2025, and adds new provisions. The sales pitch is simple: lower taxes for American families. The reality is more complicated, and the complication is where they hope you stop reading.

Here is what the bill does. It raises the state and local tax (SALT) deduction cap from ten thousand dollars to forty thousand dollars, which sounds great until you realize that the benefit lands almost entirely on higher-income homeowners in high-tax states. It bumps the standard deduction by $350 for single filers and $700 for joint filers, which is real but modest. It adds a temporary deduction of up to $6,000 for seniors, expiring in 2028. It exempts tips and overtime from federal income tax, which is a genuine relief for service workers and tradespeople.

And then the bill pays for part of it by cutting roughly 1.4 trillion dollars over a decade from Medicaid, the Supplemental Nutrition Assistance Program (food stamps), and federal student loan programs. The Congressional Budget Office estimates that 10.9 million more Americans will be uninsured by 2034 as a direct result, with 7.8 million of those losses attributable to Medicaid cuts.

The CBO scored the bill. Depending on which estimate you use, static or dynamic, the Big Beautiful Bill adds between 2.4 and 3.4 trillion dollars to the federal deficit over the next decade. It cuts spending by nearly 1.3 trillion over 10 years. It reduces revenue by nearly 3.7 trillion. The gap between those two numbers is the bill you are not being shown.

WHO ACTUALLY PAYS LESS? THE ANSWER MIGHT RUIN YOUR DAY.

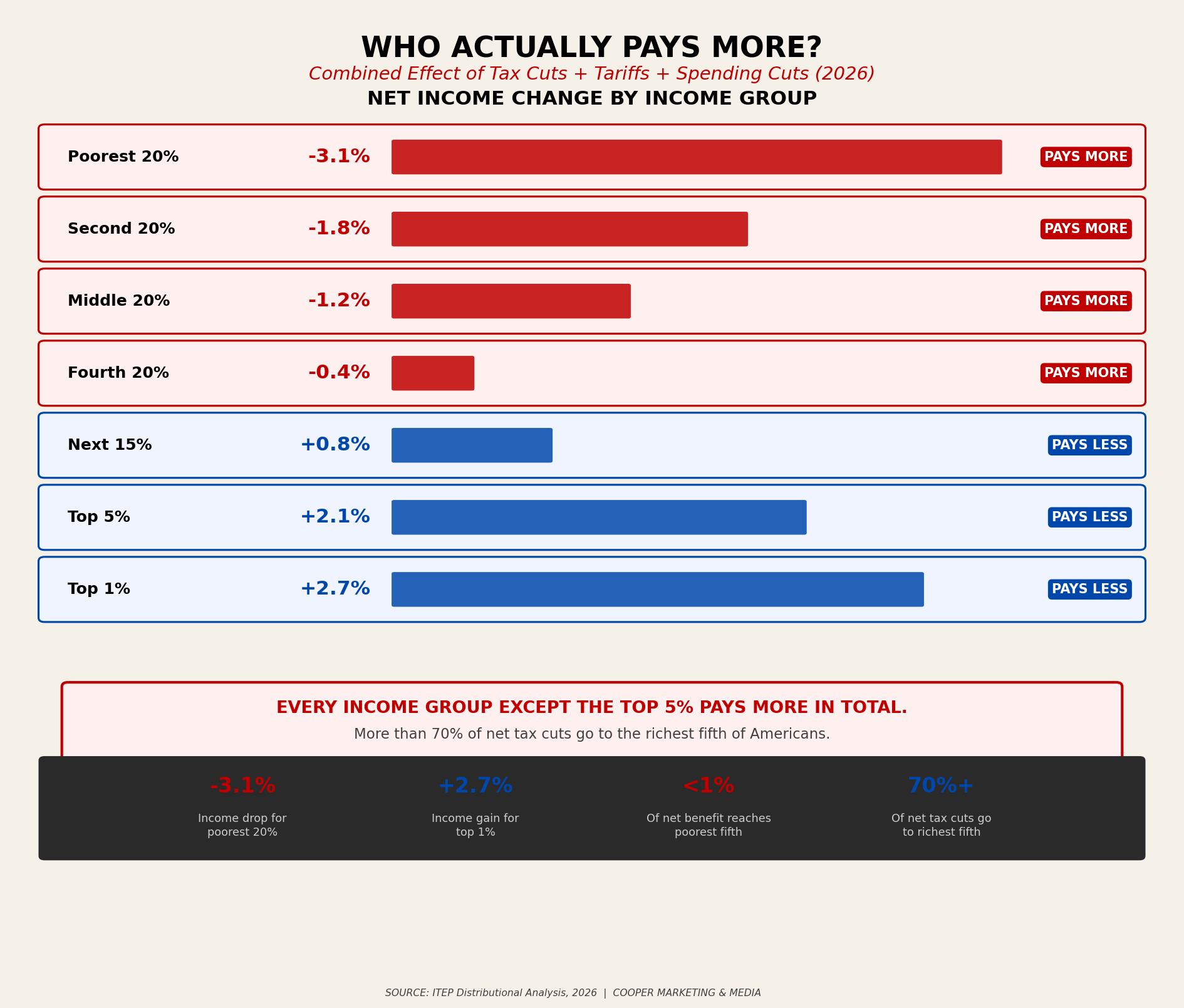

This is the part that requires you to sit still for a minute and think like an accountant, not a fan. The Institute on Taxation and Economic Policy (ITEP) ran a distributional analysis of the combined effects of the Big Beautiful Bill and current tariff policy in 2026. The findings are not subtle.

The combined impact of these policies in 2026 is a net tax increase for the average American in every income group except the richest five percent. Read that again. Every income group except the top five percent pays more in total. The richest one percent, in particular, receives a noticeable tax cut compared to everyone else. More than 70% of net tax cuts go to the richest fifth of Americans. Only ten percent of the net benefit reaches the middle fifth. Less than one percent goes to the poorest fifth.

The bottom 40% of Americans face a tariff bill larger than any tax cut they receive under the new law. For the middle twenty percent, income drops by an average of 1.2 percent. The lowest 10 percent of earners see their income fall by 3.1 percent, mostly due to cuts to Medicaid and food aid. The top 10 percent see their income rise by 2.7 percent, mostly from tax cuts.

This is what "lower taxes" looks like when you open the envelope rather than just read the headline.

THE TALKING POINTS VS. THE FINE PRINT

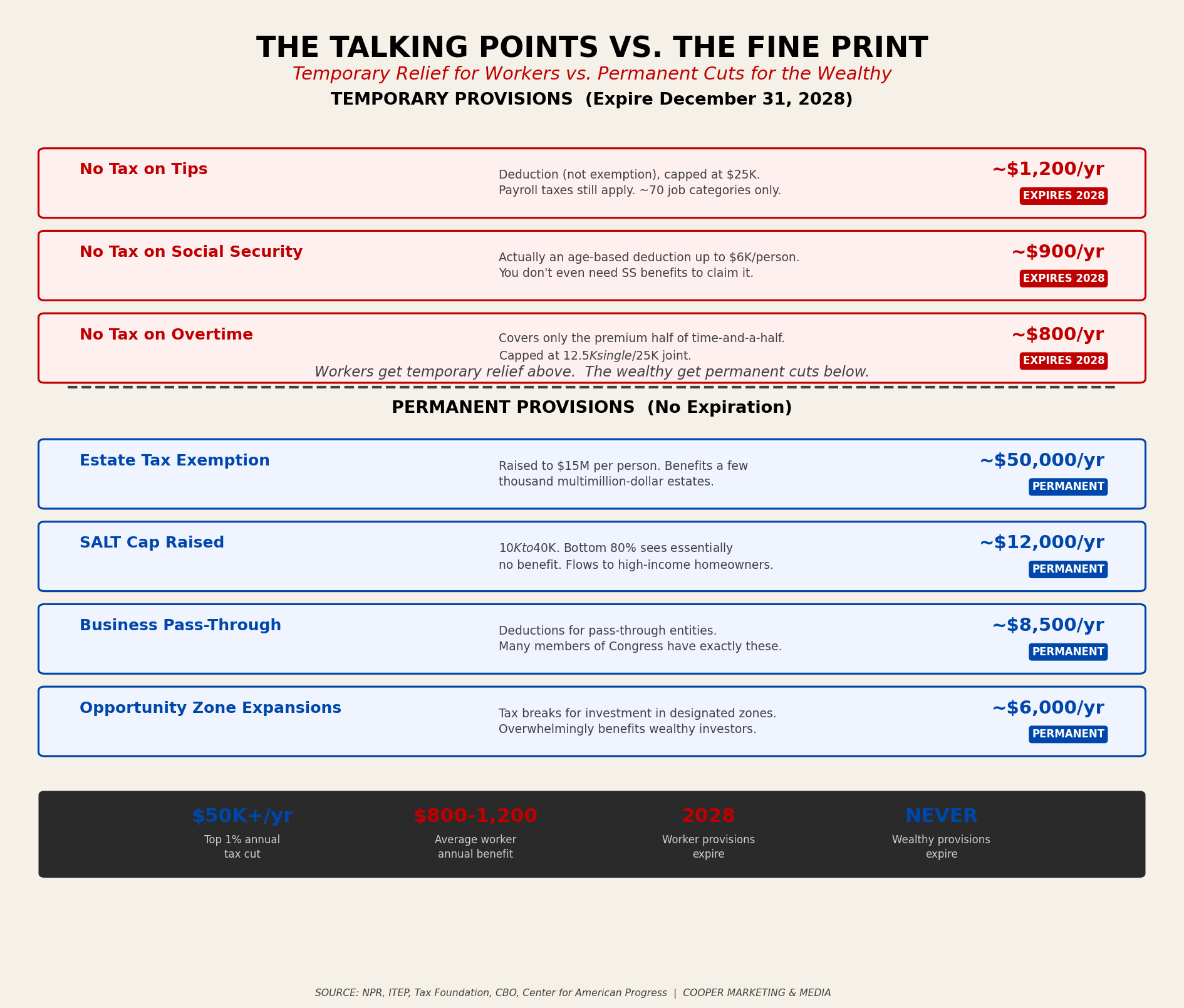

Let us deal with the three phrases the administration has been repeating on every cable show, every social post, every rally stage, and every podcast mic they can find. No tax on tips. No tax on Social Security. No tax on overtime. These are the shiny objects. They are designed to end the conversation before it starts. They sound enormous. They are not.

No tax on tips. What actually passed is a federal income tax deduction, not an exemption, capped at $25,000 per year of qualified tip income. It applies only to workers in occupations listed in a final IRS regulation, roughly seventy job categories from bartenders to water taxi operators. It does not cover automatic gratuities, service charges, or mandatory tips. It does not cover tips earned in law, medicine, or other so-called Specified Service Trades. And here is the part nobody says on television: the tips are still subject to payroll taxes, meaning Social Security and Medicare taxes still come out of every dollar. If your server earns twenty thousand in tips this year, the income tax deduction helps. The 7.65 percent payroll tax still hits. Oh, and the whole provision expires on December 31, 2028.

No tax on Social Security. What actually passed is not an exemption from Social Security benefits. It is an additional standard deduction for taxpayers age 65 and older, worth up to $6,000 per person. If you are married and filing jointly and both of you qualify, that is up to $12,000. It phases out for single filers above seventy-five thousand in income and joint filers above a hundred and fifty thousand. It expires in 2028. You do not even need to receive Social Security benefits to claim it. It is an age-based deduction from the Social Security cost. The administration says it shields roughly 90% of seniors from paying federal income tax on their benefits, which may be true in the narrow sense that many seniors already pay little or no federal income tax on those benefits. The deduction did not create that math. It just took credit for it.

No tax on overtime. What actually passed is a deduction that covers only the premium half of time-and-a-half pay, not the base rate for those overtime hours. It is capped at $12,500 for single filers and $25,000 for joint filers. It phases out at an income of 150,000. It applies only to non-exempt W-2 employees whose overtime qualifies under federal labor law. And it expires, like the others, on December 31, 2028.

Notice the pattern. All three provisions are temporary. All three are deductions, not exemptions. All three have income caps that phase them out for higher earners, which sounds progressive until you remember that the permanent provisions in the same bill, the estate tax exemption raised to fifteen million dollars per person, the SALT cap raised to forty thousand, the business pass-through deductions, the opportunity zone expansions, flow overwhelmingly to the wealthiest Americans. NPR reported that the top 1% receives more than $50,000 a year in tax cuts under this bill. The bottom eighty percent sees essentially no benefit from the SALT increase. The estate tax provision benefits the heirs of a few thousand multimillion-dollar estates. Those provisions do not expire. The ones for tip workers, servers, and retirees do. Read that sentence twice.

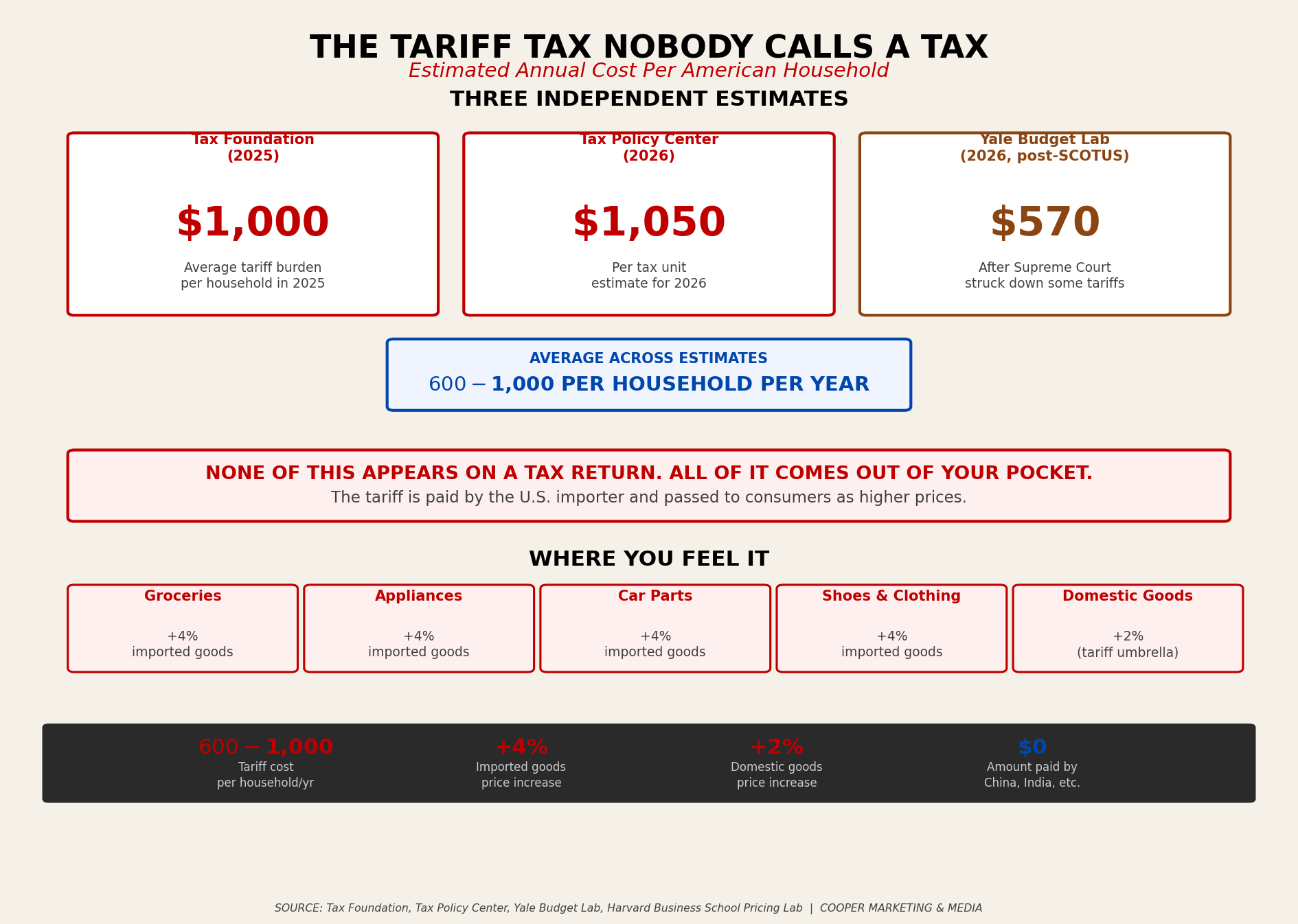

THE TARIFF TAX NOBODY CALLS A TAX

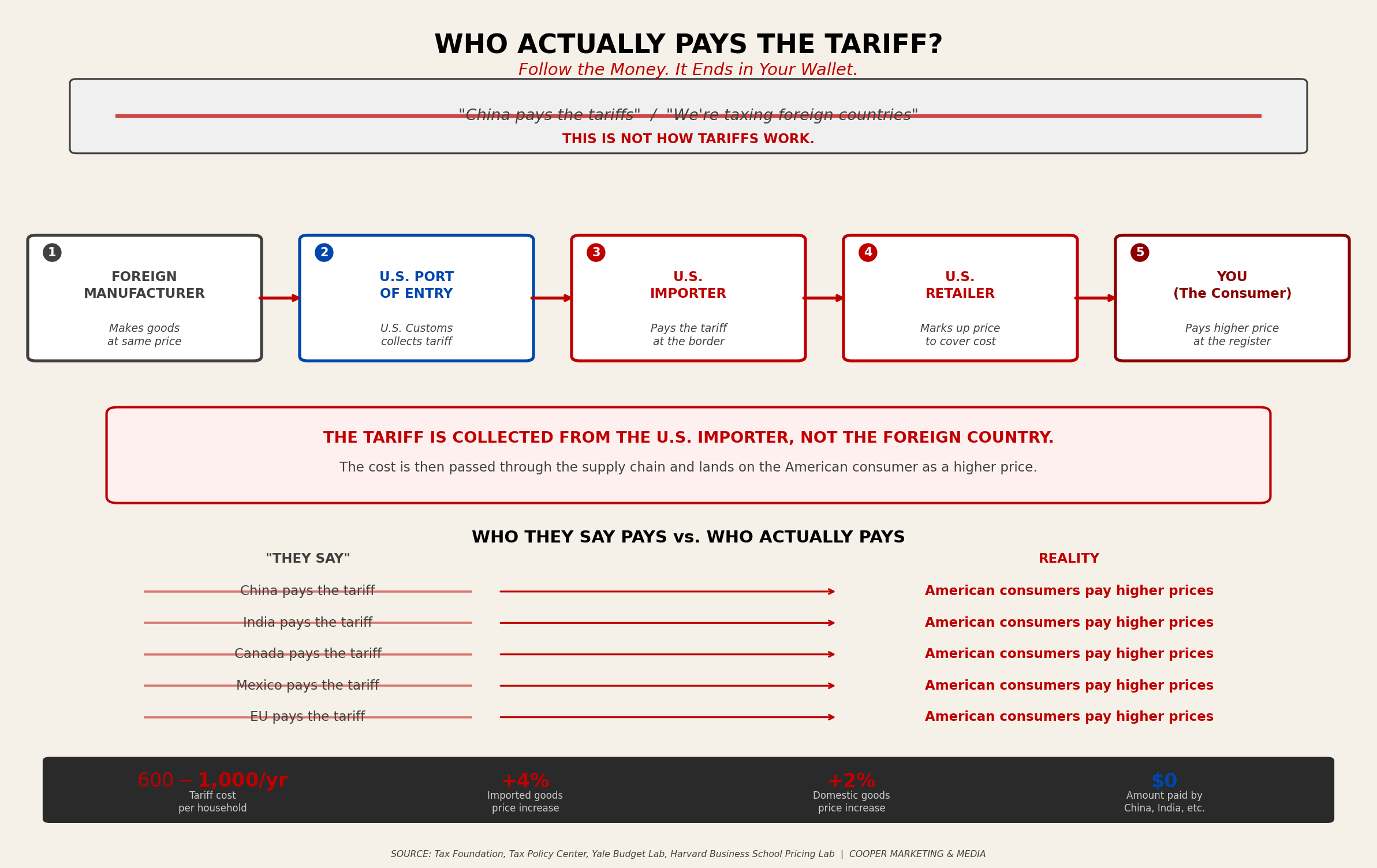

The tariff conversation is where the real sleight of hand lives. Tariffs are not paid by China. Tariffs are not paid by Europe. Tariffs are paid by American importers, who pass the cost directly to American consumers at the register. This is not an opinion. This is how tariffs have worked since the founding of the republic, and every economist left, right, and center will tell you the same thing after the third beer.

The Tax Foundation estimates that tariffs imposed through 2025 resulted in an average tax increase of roughly $1,000 per household in that year alone. The Tax Policy Center pegs the 2026 burden at about 1,050 dollars per tax unit. The Yale Budget Lab, after accounting for the Supreme Court’s February 2026 ruling that struck down some of the more aggressive tariffs, estimates a lower figure of around 570 dollars per household for 2026. Split the difference, and you are looking at somewhere between six hundred and a thousand dollars a year in costs that show up in the price of your groceries, your appliances, your car parts, and your kid’s shoes. None of this appears on a tax return.

All of it comes out of your pocket.

The Harvard Business School Pricing Lab found that the price of imported goods rose about four percent between March and September 2025, while domestic goods rose two percent. The tariffs did not make foreign goods cheaper. They made American goods more expensive, too, because domestic producers saw the tariff wall and raised their own prices behind it. That is what economists call a "tariff umbrella," and it is exactly as unpleasant as it sounds.

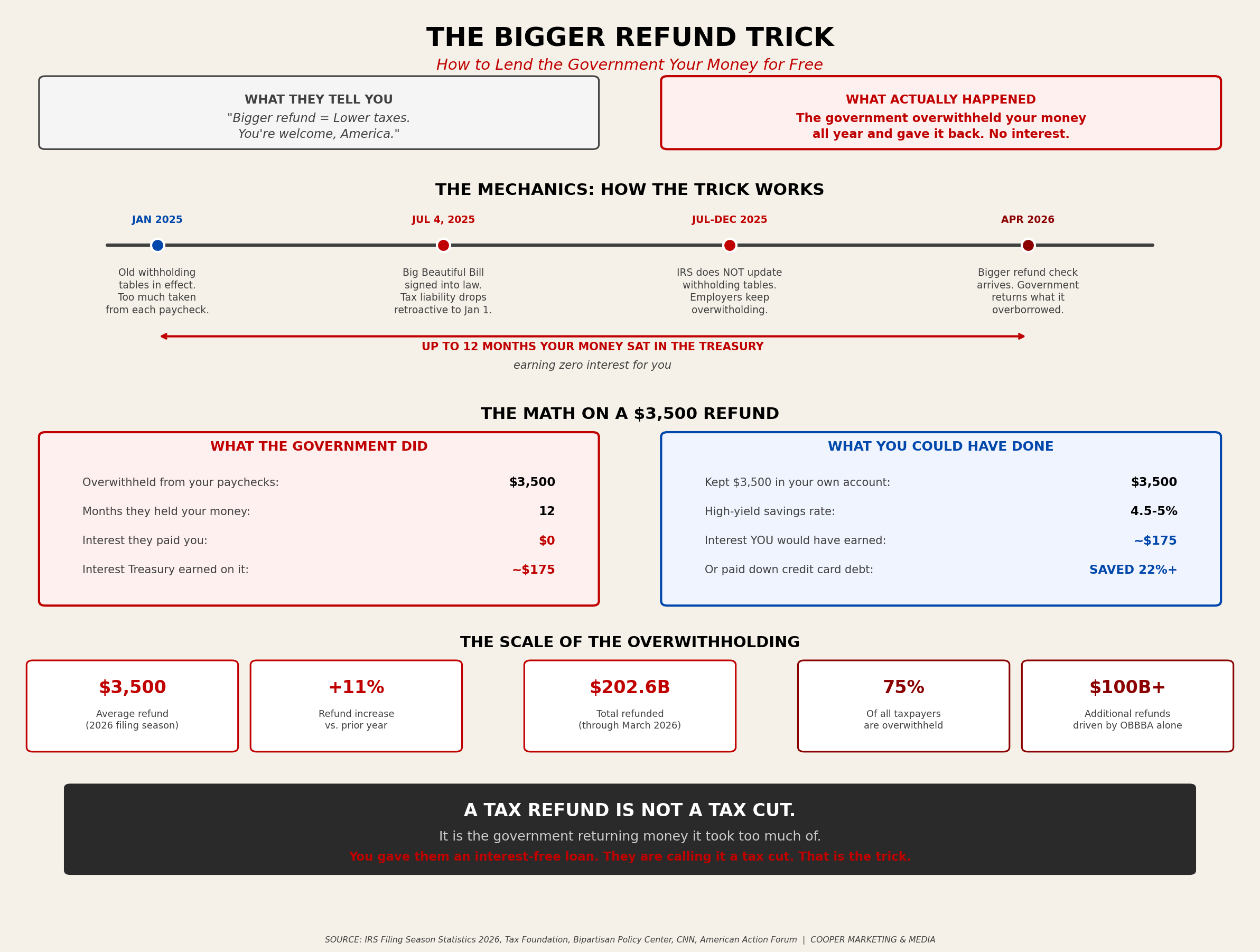

THE BIGGER REFUND TRICK, OR: HOW TO LEND THE GOVERNMENT YOUR MONEY FOR FREE

Now for the one that really needs explaining, because this is the talking point doing the heaviest lifting right now. Bigger tax refunds. The average refund in the 2026 filing season is running at roughly $3,500, up almost 11% from the same point last year, according to IRS filing data through March. As of March 20, the IRS had refunded $202.6 billion, up from $179.5 billion at the same point in 2025. The Ways and Means Committee is victory-lapping. The social posts are writing themselves. See? Lower taxes. Bigger refunds. You are welcome, America.

Allow me to mansplain what a tax refund actually is, since the people using it as a talking point are counting on you not knowing.

A tax refund is not a gift. A tax refund is not a bonus. A tax refund is not the government giving you money. A tax refund is the money the government gives you back that it took from you during the year. That is it. That is the whole thing. When your employer withholds federal income tax from every paycheck, the amount withheld is based on IRS withholding tables. If the amount withheld over twelve months exceeds your actual tax liability, the government owes you the difference. That difference is your refund. You overpaid. They are returning the overpayment. No interest.

Let me say that part again. No interest. The U.S. Treasury held your money for up to twelve months, used it however it wanted, and returned it to you without a single cent of interest. If you had kept that money in your own pocket and put it in a high-yield savings account earning four and a half to five percent, a thirty-five-hundred-dollar overpayment would have earned you roughly a hundred and seventy-five dollars in interest over the year. Instead, the government earned that interest. You got a check in April and felt grateful. That is the trick.

Now here is why the 2026 refunds are especially large, and this part matters. The One Big Beautiful Bill was signed on July 4, 2025, with its tax provisions retroactive to January 1, 2025. But the IRS did not update its withholding tables for the rest of 2025. That means your employer kept withholding taxes at the old, higher rate for the entire year, even though your actual tax liability had gone down. The result is a massive overwithhold across the entire workforce. The Tax Foundation, the Bipartisan Policy Center, and CNN have all reported this explicitly. The bigger refund is not evidence that you are paying less in taxes. The bigger refund is evidence that the government borrowed more of your money, interest-free, because the IRS was slow to update the tables after the law changed.

The U.S. Treasury estimates that nearly three-quarters of all taxpayers are overwithheld in a typical year. In 2025, that over-withholding was significantly worse due to the mid-year law change. Private-sector estimates suggest the OBBBA alone is driving up to a hundred billion dollars in additional refunds this filing season, with individual refunds up by between three hundred and a thousand dollars compared with a normal year. All of that is money that sat in the Treasury’s accounts earning nothing for you while you paid interest on your credit card, your car loan, or your mortgage.

So the next time someone points to a bigger refund check as proof of lower taxes, here is what you say. That check is my own money. The government held it for 12 months without my permission and without paying me interest. If I had kept it in my own account, I would have earned $175. Instead, the government earned that yield, and now I am supposed to thank them for returning what they overborrowed. That is not a tax cut. That is a float, and Wall Street has a word for making money off other people’s float. It is called a business model.

WHO IS REALLY CASHING IN? BOTH SIDES OF THE AISLE.

I am going to say something that will irritate everyone equally, which is usually a sign that it is accurate. This is not just a Republican problem. It is a bipartisan grift hiding behind partisan theater.

Every member of Congress who voted for this bill and owns real estate in a high-tax state just gave themselves a larger SALT deduction. Every member with a business structured as a pass-through entity, and many of them have exactly that, benefits from the pass-through provisions. Every member with an estate worth more than fifteen million dollars, or whose donors have estates worth that, is just locked in a permanent tax shelter for generational wealth. That is not hypothetical. That is the text of the law they signed.

On the other side, every Democratic member who stayed quiet on the tariff regime because opposing tariffs is politically inconvenient in an election year is complicit in the hidden tax on working families. Every elected official who accepted campaign contributions from the industries benefiting most from the bill and then issued a stern press release without voting to amend a single provision is performing opposition, not practicing it.

This is a bipartisan accountability problem. The only people not cashing in are the ones writing the checks, and that is you.

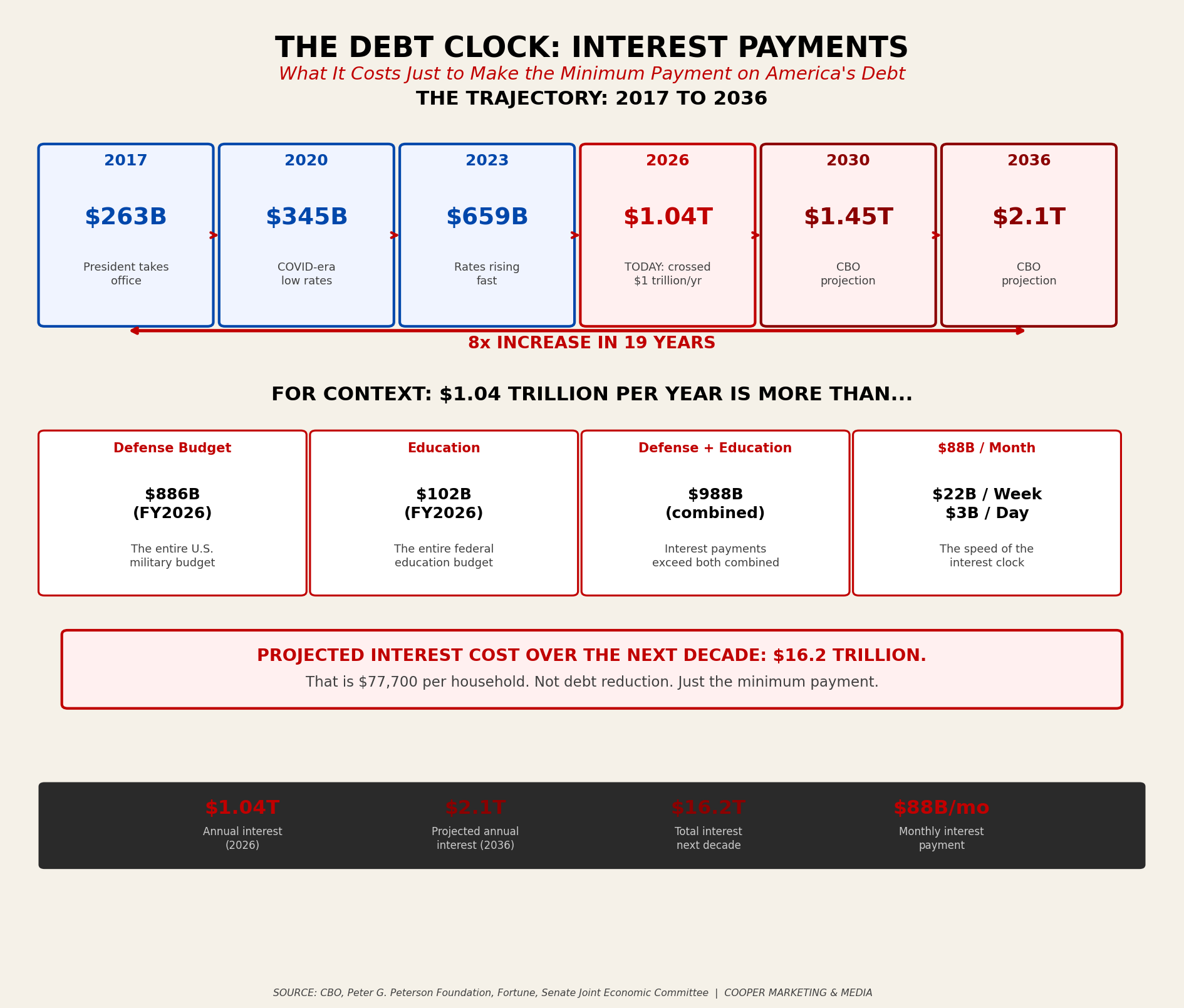

THE DEBT CLOCK AND THE SOUND IT MAKES AT 3 A.M.

Here is where we zoom out, and where the math turns from annoying to existential.

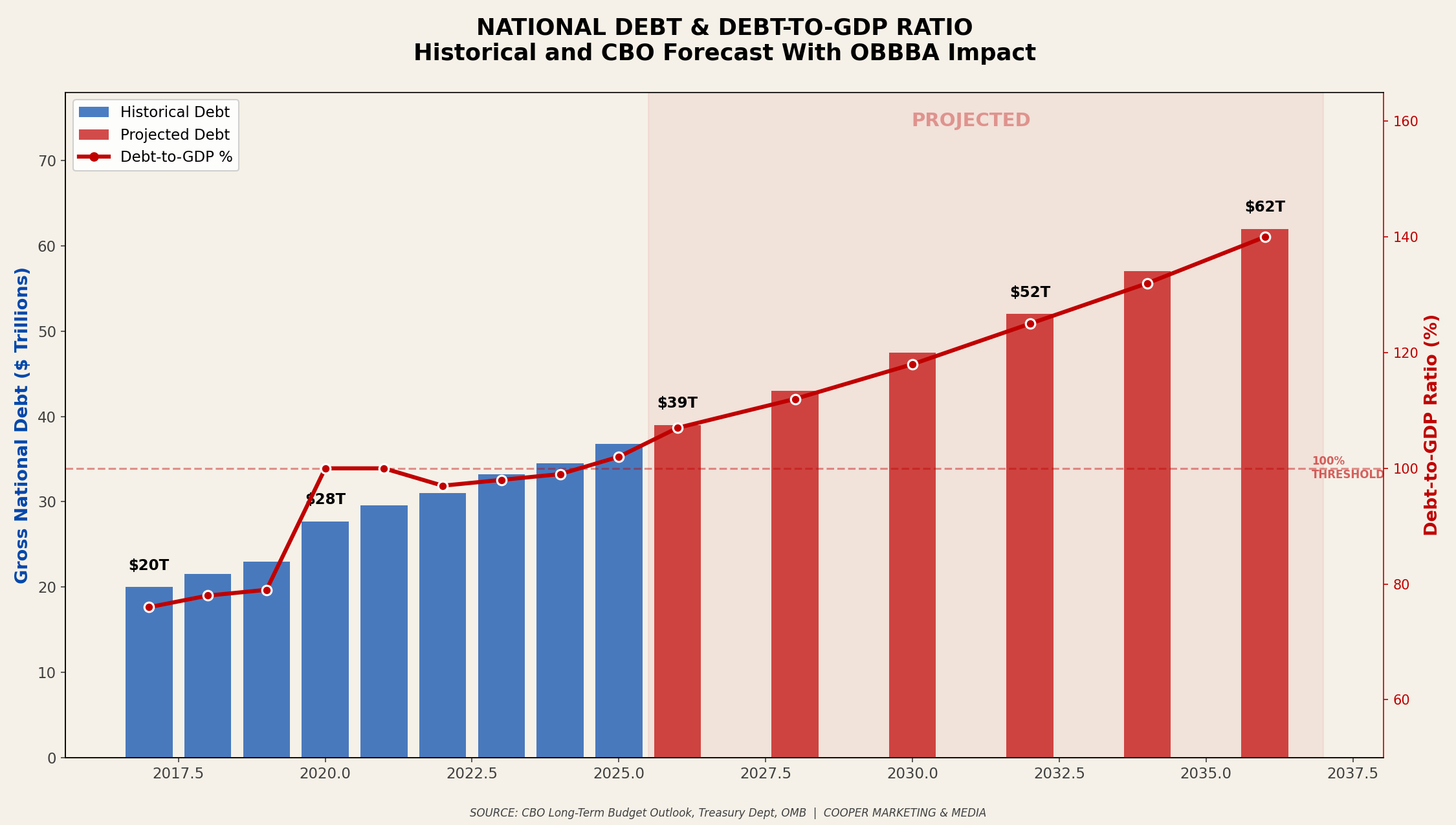

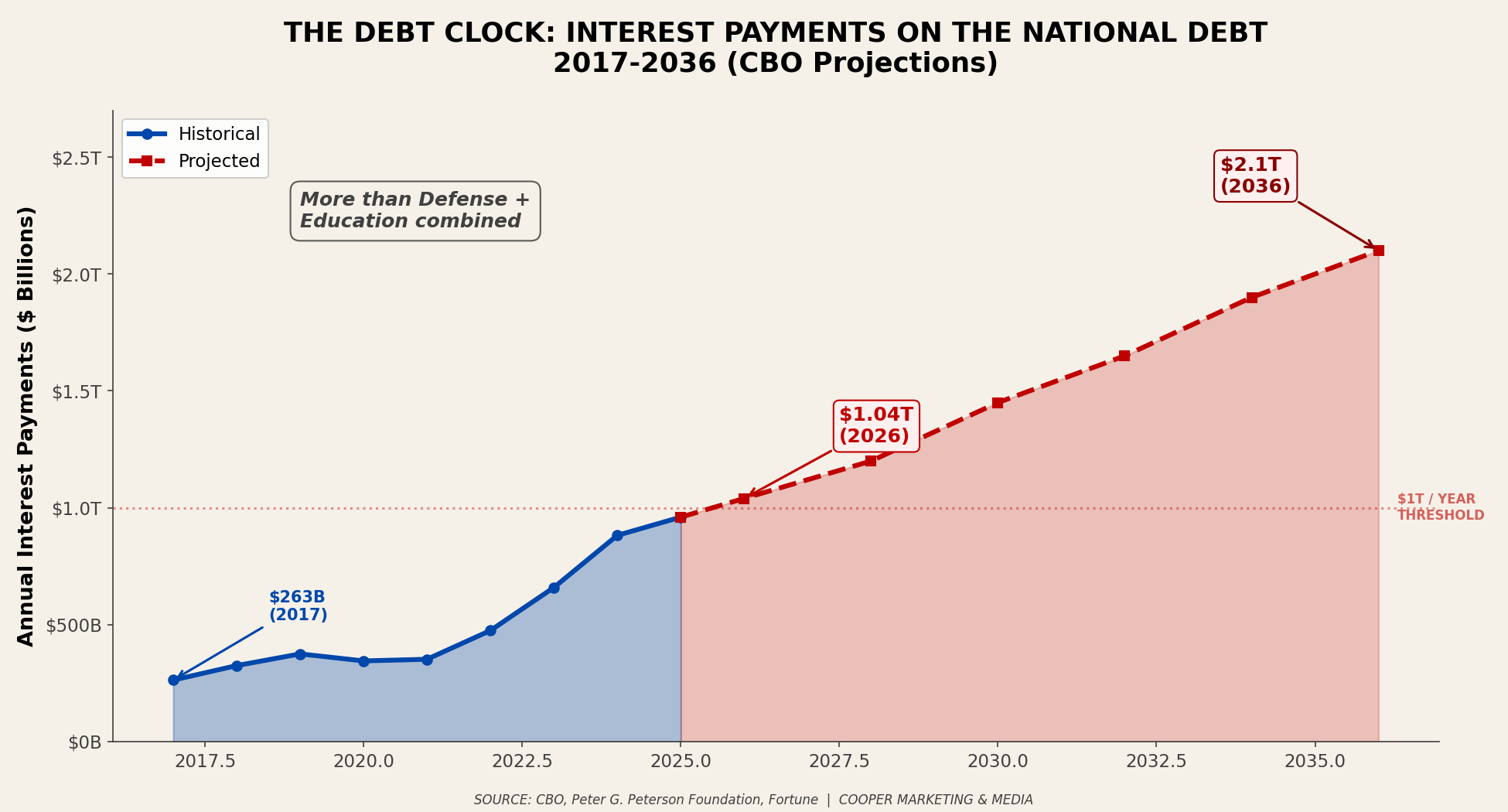

The gross national debt of the United States crossed thirty-nine trillion dollars on March 17, 2026. That is up from 34.5 trillion just two years earlier, an increase of 4.5 trillion dollars in twenty-four months. The debt was roughly twenty trillion when the current President first took office in January 2017. He promised to eliminate it. It has nearly doubled.

Interest payments on the national debt are projected at 1.04 trillion dollars for fiscal year 2026 alone. That is eighty-eight billion a month. Twenty-two billion a week. More than three billion a day. The federal government is now spending more on interest than it spends on defense and education combined. One trillion dollars a year, every year, just to service the debt, not reduce it, not pay it down, just to make the minimum payment. That is projected to rise to 2.1 trillion a year by 2036. The CBO projects total interest costs of 16.2 trillion dollars over the next decade.

Put that in household terms. Each American household’s share of the interest bill alone is roughly $7,700 a year. Not the debt. Just the interest. That is not a tax cut. That is a credit card bill being forwarded to your children.

ARE WE ON A COLLISION COURSE?

Let us apply the Pinker test. Strip out the tribal signaling. Ignore the rally chants. Ignore the counter-chants. Just look at the ledger.

Revenue is being cut by 3.7 trillion over a decade. Spending is being cut by 1.3 trillion. The gap is roughly 2.4 trillion in new deficit, and that is the optimistic CBO number. The dynamic estimate puts it at 3.4 trillion. Meanwhile, the debt is growing at seven billion dollars a day, interest is eating a trillion a year, the tariff regime is functioning as a hidden regressive tax on working families, and the tax cuts themselves flow disproportionately to the wealthiest five percent.

If a private company presented those numbers to a board of directors, the board would fire the CFO before lunch.

This is not about left or right. This is about math. Fiscal conservatives, the real ones, the ones who balanced checkbooks on Sunday morning and believed government should live within its means, should be the loudest voices in the room right now. The people who promised you discipline are spending like lottery winners with a drinking problem. The bill is on the table. It has your name on it.

WHAT YOU CAN DO, AND WHAT YOU MUST

Read the CBO score yourself. It is public, free, and available at cbo.gov. Run the ITEP numbers for your own state at itep.org. Look at your grocery bills from last year and this year, and do the tariff math in your own kitchen.

Then pick up the phone. I am serious. Call your representative. Call your senator. It does not matter if they are a Republican, a Democrat, or whatever RFK Jr. is calling himself this week. Ask one question: how are we going to pay for this? If the answer is "growth," ask them to show you the growth projections from an independent source, not the administration’s own estimate, which has been disputed by CBO repeatedly. If the answer is "we cut waste," ask them to name which fifteen-million-dollar monument they are willing to cancel. If the answer is a talking point about tips or overtime, read them the fine print from this Op-Ed and ask again. Then email them. Then show up at the town hall. Then call again. These people work for you.

They forget that between elections. Remind them.

Call them to the mat. Both parties. Every single one of them who voted for a bill that cuts taxes permanently for estates worth fifteen million dollars, while giving your server a temporary deduction that expires in 2028. Every one of them who rubber-stamped a tariff regime that functions as a hidden sales tax on groceries and shoes. Every one of them who looked at a thirty-nine-trillion-dollar debt, a trillion dollars a year in interest, and a 2.4-to-3.4-trillion-dollar hole in the ten-year budget, and said, "This is fine." Name them. Call them. Hold them accountable. That is not partisan. That is citizenship.

THE ELECTION AHEAD, AND THE ONLY OPINION THAT MATTERS

We have an election coming. There is always an election coming. And here is my opinion, stated plainly, as this is an Op-Ed and I am entitled to one.

I do not care who wins. I did not care who won in 2024, and the current President won that election fair and square, and I respect the result. What I care about, the only thing I care about in this context, is that you vote. If you show up and pull the lever for higher taxes on working families, a permanently inflated deficit, and a national debt that your grandchildren will still be servicing, that is your right as an American, and I will defend it. Democracy means you get to choose, even when I think you are choosing wrong.

But here is my caveat, and I am inserting it right here where it belongs. Do the math first. Do it quickly, because the numbers are moving fast and none of them are moving in your favor. Then, once you have done the math, pick up the phone. Call your elected officials. Email them. Write them a letter on actual paper if you have to. Call them out. Call them to the mat. Because in my humble opinion, which I am expressing freely in this free country on this free internet that is still mostly full of bots and rage bait, they are not making America great again. They are fleecing your pockets. They are weakening our economy. They are undermining the fiscal foundation of the republic. And they are doing it while smiling at a rally, telling you you are paying less.

You are not paying less. The math says so. The CBO says so. The ITEP says so. The grocery receipt in your kitchen says so. The only people paying less are those who were already paying the least relative to their income, and they are paying less permanently, while your relief expires in 2028.

And here is the quiet part, the Dalai Lama’s contribution to the spreadsheet. Be compassionate with the people around you who believed the pitch. They were told they would pay less. They were told the deficit would shrink. They were told the debt would go down. None of that has happened, and admitting it does not make them wrong for hoping. It makes them human. The con is not on the voter. The con is on the ledger. Direct your energy at the ledger, and at the people who wrote it.

Now go check the numbers. Then go vote. I will wait. Again.

Coop - Sentient | Planet Earth

SOURCES & REFERENCES

• Congressional Budget Office, “Estimated Budgetary Effects of H.R. 1, the One Big Beautiful Bill Act,” June 2025 (static and dynamic scores).

• Tax Foundation, “Big Beautiful Bill House GOP Tax Plan: Preliminary Details and Analysis,” 2025.

• Institute on Taxation and Economic Policy (ITEP), “State-by-State Estimates of the First Year of Trump’s Tax Policies: All But the Richest Americans Face Higher Taxes,” 2026.

• ITEP, “Despite Any Refunds, You’re Probably Paying More Taxes Under Trump While Richest Pay Less,” 2026.

• Tax Policy Center, “TPC Tariff Tracker,” updated 2026.

• Yale Budget Lab, “Where We Stand: Fiscal, Economic, and Distributional Effects of All U.S. Tariffs Enacted in 2025,” 2025.

• Harvard Business School Pricing Lab, imported and domestic goods price analysis, 2025.

• Fortune, “The U.S. government is spending $88 billion a month in interest on national debt,” April 9, 2026.

• Fortune, “The national debt just crossed $39 trillion,” March 18, 2026.

• U.S. Senate Joint Economic Committee, “National Debt Reaches $38.86 Trillion, Increased $2.64 Trillion Year over Year,” March 2026.

• NOTUS, “Trump Will Fund New Archway With $15 Million From the National Endowment for the Humanities,” 2026.

• CBS News, “Taxpayers will help fund Independence Arch, or so-called Arc de Trump, plans indicate,” 2026.

• CNBC, “Trump’s 250-foot triumphal arch would loom over Potomac, new renderings show,” April 10, 2026.

• PBS NewsHour, “Breaking down Trump’s Big Beautiful Bill and its impact on the deficit and national debt.”

• Committee for a Responsible Federal Budget, “Trump CEA Projections Tracker” and FY 2027 budget overview.

• Peter G. Peterson Foundation, “Monthly Interest Tracker: National Debt,” 2026.

• IRS, “Treasury, IRS issue final regulations listing occupations where workers customarily and regularly receive tips under OBBBA,” April 2026.

• IRS, “One, Big, Beautiful Bill: How to take advantage of no tax on tips and overtime,” 2026.

• CNBC, “IRS publishes list of occupations that qualify for no tax on tips provision,” April 13, 2026.

• Tax Foundation, “How Does the Additional Senior Deduction Compare to No Tax on Social Security?” 2025.

• H&R Block, “One Big Beautiful Bill: No Tax on Overtime pay explained (2025-2028),” 2026.

• NPR, “Here are 6 Beautiful Bill tax changes that will benefit wealthy Americans,” November 5, 2025.

• Center for American Progress, “7 Ways the Big Beautiful Bill Cuts Taxes for the Rich,” 2025.

• CNBC, “Top five tax changes for the wealthy in Trump’s big beautiful bill,” July 3, 2025.

• Tax Foundation, “Why Is My Tax Refund Larger This Year?” and “Tax Refunds and the One Big Beautiful Bill Act,” 2026.

• Bipartisan Policy Center, “What’s Driving Higher Tax Refunds in 2026?” 2026.

• CNN, “Why federal tax refunds may be bigger than usual,” January 26, 2026.

• IRS, “Filing season statistics for week ending March 20, 2026.”

• Money, “Why Tax Refunds Will Probably Be Bigger in 2026: Withholding,” 2026.

• American Action Forum, “This Year’s Higher Tax Refunds: What’s Driving Them,” 2026.